Try picturing this for a moment.

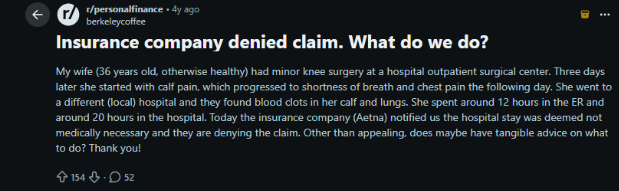

A man sits at home scrolling through a message from his insurance company, still a little unsettled by the last few days. His wife is 36, healthy, and had what everyone described as minor knee surgery at an outpatient center. Routine, they said.

Three days later the calf pain began. Then came shortness of breath. Soon after, chest pain. They rushed to a nearby hospital where doctors eventually discovered blood clots in both her calf and lungs. Roughly twelve hours passed in the ER, followed by nearly twenty more under observation. One of those long hospital days that stretch further than expected.

Will the insurance company actually pay this claim?

Then the notification arrives: the hospital stay was not medically necessary. Claim denied.

That is usually the moment insurance stops feeling like an abstract financial product and becomes something far more personal. A bit uncomfortable too.

People pay for life insurance or health insurance policies for years. Sometimes decades. Most of the time nothing happens. Which, honestly speaking, is good thing.

Yet the first time a claim becomes necessary, one quiet question begins to matter more than anything else.

How likely is the insurer to actually settle it?

This is where the Claim Settlement Ratio enters the conversation. Look up insurance in India and you will see it everywhere. Agents mention it quickly. Comparison websites display it prominently. Buyers tend to latch onto it because it feels simple – A number. A percentage. Clean, easy.

But like most financial metrics, that simplicity fades once you move closer.

We at Fianajo will help you understand how the number works underneath makes it far more useful.

At its simplest level, the Claim Settlement Ratio (CSR) represents the percentage of claims an insurance company settles compared with the total number of claims it receives within a year.

The formula itself is fairly straightforward.

| Component | Value |

| Total number of claims received | 10,000 |

| Number of claims settled | 9,500 |

| Formula used | (Claims Settled ÷ Total Claims Received) x 100 |

| Calculation | (9,500 ÷ 10,000) x 100 |

| Claim Settlement Ratio | 95% |

Which essentially means the insurer approved 95 out of every 100 claims submitted during that period.

Sounds reassuring. Most people react that way.

Numbers like this are precisely why insurers highlight claim settlement ratios in brochures and marketing material. A high percentage signals reliability quickly.

Still, the figure deserves slightly closer look before it becomes the deciding factor.

In life insurance, a claim typically arises after the policyholder passes away during the policy term.

At that point the nominee submits claim to the insurer along with the necessary documentation. Usually this includes the death certificate, policy document, identity proof of the nominee, and sometimes medical records depending on situation.

The insurer then reviews the claim in detail.

If the disclosures made when the policy was purchased align with the policy conditions, and everything appears consistent, the company releases the sum assured to the nominee.

Imagine a life insurance company receives 1,000 death claims in a financial year.

Out of those:

That leads to the following calculation.

970 ÷ 1,000 x 100 = 97 percent

That percentage becomes the company’s claim settlement ratio.

From a buyer’s perspective it feels like quick measure of trust. A shorthand for how often the insurer keeps its promise.

Reality, of course, rarely behaves quite that neatly.

Health insurance claims function a little differently.

Unlike life insurance, where a claim usually happens once, health insurance claims can occur many times during a policyholder’s life. Hospitalization, surgeries, treatments. Small claims. Large claims.

Because of this, health insurers process enormous volumes of claims every year. Thousands. Often lakhs.

For example, suppose a health insurance company receives 50,000 claims in a year and settles 47,500 of them.

| Component | Value |

| Total number of claims received | 50,000 |

| Number of claims settled | 47,500 |

| Formula used | (Claims Settled ÷ Total Claims Received) x 100 |

| Calculation | (47,500 ÷ 50,000) x 100 |

| Claim Settlement Ratio | 95% |

The formula remains exactly the same. What changes is the nature of the claims themselves.

Another detail worth noting. Health insurance claims are sometimes only partially settled. The insurer may approve portion of the claim depending on policy coverage, exclusions, or room rent limits.

So technically a claim might still be classified as “settled” even if the entire requested amount was not paid. Small detail perhaps. Still important one.

In India, the most reliable claim settlement data usually comes from the Insurance Regulatory and Development Authority of India (IRDAI).

IRDAI acts as the regulator overseeing the insurance industry. Each year it publishes detailed reports containing statistics across life insurers, health insurers, and general insurance companies.

These reports include claim settlement ratios for different insurers. Many financial websites and comparison platforms simply pull numbers directly from IRDAI publications.

According to recent data, the life insurance industry settled roughly 97.1 percent of individual death claims within 30 days during FY 2024-25.

A few insurers even reported settlement ratios exceeding 99 percent during the same period. Which sounds almost perfect, at least on paper.

Numbers like these naturally create confidence. That reaction is understandable. Yet percentages sometimes hide details. Not intentionally. Just how statistics work.

People tend to like simple indicators. Especially when the topic involves something as uncertain as insurance. Buying insurance requires a small leap of faith. Premiums are paid year after year without knowing whether the policy will ever be used.

When a claim finally appears, the process becomes the real test.

Because of that uncertainty, buyers search for signals suggesting an insurer will behave responsibly when the time comes.

The claim settlement ratio gradually became one of those signals.

A high number implies the insurer approves most claims rather than rejecting them. Naturally companies highlight it. Easy metric to communicate. Still, numbers sometimes behave strangely. A statistic may be technically correct and still leave out half the story.

One subtle detail many buyers miss involves the difference between claim count and claim value. Most claim settlement ratios measure the number of claims settled rather than the total amount of money paid out.

That distinction matters more than it first appears.

Industry data suggests the insurance sector’s claim settlement ratio by count sits around 98.32 percent, while the ratio measured by claim value drops slightly to roughly 97.18 percent.

The gap is small, yet it hints at something interesting.

Rejected claims often involve larger claim amounts.

In other words, insurers may settle many smaller claims while examining larger payouts more carefully. Makes sense if you think about it.

Larger payments usually invite deeper scrutiny.

Recent statistics from IRDAI and financial publications provide clearer sense of how claims are handled in India.

For life insurance:

Health insurance data reveals broadly similar pattern, though with slightly more variation.

Some insurers such as Acko, Aditya Birla Health Insurance, and Niva Bupa recorded strong claim settlement performance in recent IRDAI data.

At the same time, a few insurers reported settlement ratios below 90 percent. Analysts usually interpret that as weaker performance. Another statistic quietly illustrates the scale of the industry. Health insurers process crores of claims every year across India.

Which means behind every percentage point sits enormous number of individual cases – People. Families. Hospitals. Paperwork.

It is also worth acknowledging something slightly uncomfortable but true. Not every rejected claim is unfair.

Insurance policies operate under clearly defined conditions. If those conditions are violated, the insurer may legally reject claim.

Some of the most common reasons include:

Non disclosure of medical history

Incorrect information in the proposal form

Policy lapse due to unpaid premiums

Waiting period restrictions

Treatment for excluded illnesses

Consider a simple example.

Someone purchases policy but chooses not to disclose an existing medical condition during the application process. Years later a claim arises related to that same condition.

After investigation the insurer may reject claim because the original disclosure was incomplete.

This is why advisors repeat the same piece of advice again and again. Be honest while buying insurance. Full disclosure at beginning usually prevents complicated disputes later.

So how should someone actually use the claim settlement ratio while comparing insurers?

The simplest approach is to treat it as one indicator among several.

If a company has unusually low claim settlement ratio, that might signal problems with claims handling. But once the numbers reach the mid or high nineties, differences between companies begin to shrink.

For instance, comparing 96 percent with 97 percent might not meaningfully change the experience of policyholder. At that stage other factors start to matter more.

Policy coverage. Exclusions. The hospital network available for cashless treatment. Claim processing timelines. Even customer service quality. Insurance decisions rarely come down to a single statistic.

Finanjo will help you understand claim settlement ratio, but know that it simply offers one window into how insurers behave when claims arrive. It helps. It informs conversation.

It never tells the entire story. And perhaps it was never meant to.

Try picturing this for a moment.

A man sits at home scrolling through a message from his insurance company, still a little unsettled by the last few days. His wife is 36, healthy, and had what everyone described as minor knee surgery at an outpatient center. Routine, they said.

Three days later the calf pain began. Then came shortness of breath. Soon after, chest pain. They rushed to a nearby hospital where doctors eventually discovered blood clots in both her calf and lungs. Roughly twelve hours passed in the ER, followed by nearly twenty more under observation. One of those long hospital days that stretch further than expected.

Will the insurance company actually pay this claim?

Then the notification arrives: the hospital stay was not medically necessary. Claim denied.

That is usually the moment insurance stops feeling like an abstract financial product and becomes something far more personal. A bit uncomfortable too.

People pay for life insurance or health insurance policies for years. Sometimes decades. Most of the time nothing happens. Which, honestly speaking, is good thing.

Yet the first time a claim becomes necessary, one quiet question begins to matter more than anything else.

How likely is the insurer to actually settle it?

This is where the Claim Settlement Ratio enters the conversation. Look up insurance in India and you will see it everywhere. Agents mention it quickly. Comparison websites display it prominently. Buyers tend to latch onto it because it feels simple – A number. A percentage. Clean, easy.

But like most financial metrics, that simplicity fades once you move closer.

We at Fianajo will help you understand how the number works underneath makes it far more useful.

At its simplest level, the Claim Settlement Ratio (CSR) represents the percentage of claims an insurance company settles compared with the total number of claims it receives within a year.

The formula itself is fairly straightforward.

| Component | Value |

| Total number of claims received | 10,000 |

| Number of claims settled | 9,500 |

| Formula used | (Claims Settled ÷ Total Claims Received) x 100 |

| Calculation | (9,500 ÷ 10,000) x 100 |

| Claim Settlement Ratio | 95% |

Which essentially means the insurer approved 95 out of every 100 claims submitted during that period.

Sounds reassuring. Most people react that way.

Numbers like this are precisely why insurers highlight claim settlement ratios in brochures and marketing material. A high percentage signals reliability quickly.

Still, the figure deserves slightly closer look before it becomes the deciding factor.

In life insurance, a claim typically arises after the policyholder passes away during the policy term.

At that point the nominee submits claim to the insurer along with the necessary documentation. Usually this includes the death certificate, policy document, identity proof of the nominee, and sometimes medical records depending on situation.

The insurer then reviews the claim in detail.

If the disclosures made when the policy was purchased align with the policy conditions, and everything appears consistent, the company releases the sum assured to the nominee.

Imagine a life insurance company receives 1,000 death claims in a financial year.

Out of those:

That leads to the following calculation.

970 ÷ 1,000 x 100 = 97 percent

That percentage becomes the company’s claim settlement ratio.

From a buyer’s perspective it feels like quick measure of trust. A shorthand for how often the insurer keeps its promise.

Reality, of course, rarely behaves quite that neatly.

Health insurance claims function a little differently.

Unlike life insurance, where a claim usually happens once, health insurance claims can occur many times during a policyholder’s life. Hospitalization, surgeries, treatments. Small claims. Large claims.

Because of this, health insurers process enormous volumes of claims every year. Thousands. Often lakhs.

For example, suppose a health insurance company receives 50,000 claims in a year and settles 47,500 of them.

| Component | Value |

| Total number of claims received | 50,000 |

| Number of claims settled | 47,500 |

| Formula used | (Claims Settled ÷ Total Claims Received) x 100 |

| Calculation | (47,500 ÷ 50,000) x 100 |

| Claim Settlement Ratio | 95% |

The formula remains exactly the same. What changes is the nature of the claims themselves.

Another detail worth noting. Health insurance claims are sometimes only partially settled. The insurer may approve portion of the claim depending on policy coverage, exclusions, or room rent limits.

So technically a claim might still be classified as “settled” even if the entire requested amount was not paid. Small detail perhaps. Still important one.

In India, the most reliable claim settlement data usually comes from the Insurance Regulatory and Development Authority of India (IRDAI).

IRDAI acts as the regulator overseeing the insurance industry. Each year it publishes detailed reports containing statistics across life insurers, health insurers, and general insurance companies.

These reports include claim settlement ratios for different insurers. Many financial websites and comparison platforms simply pull numbers directly from IRDAI publications.

According to recent data, the life insurance industry settled roughly 97.1 percent of individual death claims within 30 days during FY 2024-25.

A few insurers even reported settlement ratios exceeding 99 percent during the same period. Which sounds almost perfect, at least on paper.

Numbers like these naturally create confidence. That reaction is understandable. Yet percentages sometimes hide details. Not intentionally. Just how statistics work.

People tend to like simple indicators. Especially when the topic involves something as uncertain as insurance. Buying insurance requires a small leap of faith. Premiums are paid year after year without knowing whether the policy will ever be used.

When a claim finally appears, the process becomes the real test.

Because of that uncertainty, buyers search for signals suggesting an insurer will behave responsibly when the time comes.

The claim settlement ratio gradually became one of those signals.

A high number implies the insurer approves most claims rather than rejecting them. Naturally companies highlight it. Easy metric to communicate. Still, numbers sometimes behave strangely. A statistic may be technically correct and still leave out half the story.

One subtle detail many buyers miss involves the difference between claim count and claim value. Most claim settlement ratios measure the number of claims settled rather than the total amount of money paid out.

That distinction matters more than it first appears.

Industry data suggests the insurance sector’s claim settlement ratio by count sits around 98.32 percent, while the ratio measured by claim value drops slightly to roughly 97.18 percent.

The gap is small, yet it hints at something interesting.

Rejected claims often involve larger claim amounts.

In other words, insurers may settle many smaller claims while examining larger payouts more carefully. Makes sense if you think about it.

Larger payments usually invite deeper scrutiny.

Recent statistics from IRDAI and financial publications provide clearer sense of how claims are handled in India.

For life insurance:

Health insurance data reveals broadly similar pattern, though with slightly more variation.

Some insurers such as Acko, Aditya Birla Health Insurance, and Niva Bupa recorded strong claim settlement performance in recent IRDAI data.

At the same time, a few insurers reported settlement ratios below 90 percent. Analysts usually interpret that as weaker performance. Another statistic quietly illustrates the scale of the industry. Health insurers process crores of claims every year across India.

Which means behind every percentage point sits enormous number of individual cases – People. Families. Hospitals. Paperwork.

It is also worth acknowledging something slightly uncomfortable but true. Not every rejected claim is unfair.

Insurance policies operate under clearly defined conditions. If those conditions are violated, the insurer may legally reject claim.

Some of the most common reasons include:

Non disclosure of medical history

Incorrect information in the proposal form

Policy lapse due to unpaid premiums

Waiting period restrictions

Treatment for excluded illnesses

Consider a simple example.

Someone purchases policy but chooses not to disclose an existing medical condition during the application process. Years later a claim arises related to that same condition.

After investigation the insurer may reject claim because the original disclosure was incomplete.

This is why advisors repeat the same piece of advice again and again. Be honest while buying insurance. Full disclosure at beginning usually prevents complicated disputes later.

So how should someone actually use the claim settlement ratio while comparing insurers?

The simplest approach is to treat it as one indicator among several.

If a company has unusually low claim settlement ratio, that might signal problems with claims handling. But once the numbers reach the mid or high nineties, differences between companies begin to shrink.

For instance, comparing 96 percent with 97 percent might not meaningfully change the experience of policyholder. At that stage other factors start to matter more.

Policy coverage. Exclusions. The hospital network available for cashless treatment. Claim processing timelines. Even customer service quality. Insurance decisions rarely come down to a single statistic.

Finanjo will help you understand claim settlement ratio, but know that it simply offers one window into how insurers behave when claims arrive. It helps. It informs conversation.

It never tells the entire story. And perhaps it was never meant to.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.