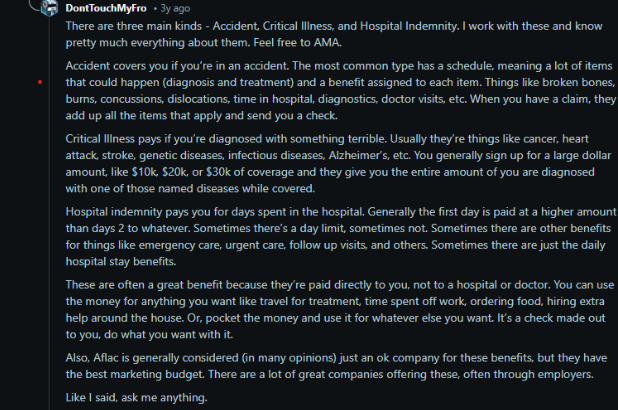

Raj had just finished buying his first term policy without riders in insurance.

For a moment it felt oddly satisfying. Not exciting exactly. But there was a quiet sense of doing something responsible, something future-looking. The agent had explained the basics well enough. Pay the premium every year, keep the policy running, and if something happened to him during the policy term, the money would go to his family. Simple enough. Predictable. The sort of thing people tell themselves they will do someday, and then keep postponing.

Raj was about to close the laptop when the agent asked one more question.

“Would you like to add riders in insurance?”

He paused. The word sounded familiar but vague. Was this another policy? A feature? Or just one of those add-ons people agree to because the difference in premium seems small in the moment.

The agent began listing them. Critical illness rider. Accidental death rider. Waiver of premium rider.

Now Raj had mixed feelings. On one hand, each rider sounded practical. Life is messy and unpredictable after all. On the other hand, it felt like the simple policy he just understood was slowly turning into a menu of decisions he was not fully sure about.

That confusion is actually very common.

Many people buy a term plan and move on without ever really understanding riders in insurance. Some add every option suggested because the additional premium feels manageable. Others avoid them completely because the details feel confusing and the policy already seems complicated enough.

Usually the answer sits somewhere in between.

Understanding what riders really do, how they connect to a base insurance policy, and when they genuinely make sense can make the entire decision process a lot clearer. Not simpler perhaps, but clearer with Finanjo – experts for personal finance in India.

A rider is an additional benefit that can be attached to an existing insurance policy.

It slightly modifies the policy by adding protection for certain situations that may not be fully covered by the main policy. In most cases this comes with an additional cost that increases the annual premium by a small amount. Sometimes very small, which is exactly why riders often look tempting at the time of purchase.

Think of it as an extension to the base policy.

The core policy continues to provide its original protection exactly as promised. The rider simply expands the coverage by addressing specific risks that could happen during the policy period.

For example, someone buying a term life insurance policy might add a rider that provides an extra payout if death occurs due to an accident. Another rider may provide money if the insured person is diagnosed with a critical illness such as cancer or a serious heart condition.

These benefits sit on top of the main policy rather than replacing it. The original life cover remains intact. The riders in insurance just create an additional safety layer.

Insurance companies sometimes describe riders in insurance as optional. Which is technically true. But the decision about whether to add them usually depends on how someone thinks about risk, money, and uncertainty.

Well, to answer our Reddit friend we have an explanation here with a simple example.

Let us circle back to Raj. Suppose Raj buys a term insurance policy with these details.

| Component | Value |

| Base policy type | Term Life Insurance |

| Sum assured | ₹1 crore |

| Policy term | 30 years |

| Annual premium | ₹12,000 |

Now imagine he adds Critical Illness Riders in insurance worth ₹10 lakh.

The policy would look something like this.

| Component | Value |

| Base cover | ₹1 crore life cover |

| Critical illness rider cover | ₹10 lakh |

| Additional rider premium | ₹1,200 per year |

| Total annual premium | ₹13,200 |

If Raj passes away during the policy term, his family still receives the full ₹1 crore from the base policy. That part does not change. Riders in insurance do not reduce the core life cover.

But if he is diagnosed with a covered critical illness while the policy is active, the rider allows him to receive the ₹10 lakh payout earlier. During his lifetime.

This payout is separate from the death benefit.

In many policies the rider amount is paid once the illness is diagnosed and confirmed under the policy conditions. After that the money can be used however the policyholder wants. Hospital bills. Recovery costs. Lost income. Even everyday expenses that slowly pile up when someone is unable to work.

Sometimes people assume health insurance will handle everything. In reality there are always costs that slip through the cracks. Recovery periods. Lifestyle adjustments. Small things that quietly become expensive.

That is where riders in insurance often start making sense.

Insurance policies usually focus on broad categories of risk.

Life insurance covers death. Health insurance covers medical treatment. Disability policies address income loss due to injury or illness. Structuring policies this way keeps things organized and easier to explain.

But real life rarely follows those neat boundaries.

Certain risks overlap. Or fall awkwardly between categories. A serious illness might require expensive treatment while also preventing someone from working for months. Sometimes longer.

Situations like these expose gaps.

For example:

These problems are not always fully covered by a single insurance policy.

Riders in insurance exist to close those small but important gaps.

Instead of forcing people to purchase several separate insurance policies, insurers allow smaller protections to be attached directly to the base policy. It simplifies things a little. Or at least tries to.

And usually the cost is lower than buying a completely separate policy.

Still, just because something is available does not mean it is necessary for everyone.

Companies in India offer several riders in insurance. Some are very common across insurers while others depend on the company and the specific policy.

A few riders appear in most life insurance plans.

This rider provides a lump sum payout if the policyholder is diagnosed with certain serious illnesses.

Typically the list includes conditions like:

The payout is triggered once the illness is diagnosed and confirmed under the policy definitions. And those definitions matter. Insurance policies tend to be very specific about what qualifies as a claim.

The money can be used for treatment costs, recovery expenses, or income replacement during the illness period. Unlike health insurance, the payout is usually not tied to hospital bills. The insured person decides how to use it.

Many policyholders find that flexibility reassuring.

Critical illness riders are probably the most widely chosen riders with term insurance policies in India.

An accidental death rider provides an additional payout if death occurs due to an accident.

Suppose the base policy provides ₹1 crore cover.

If the policyholder has an accidental death rider worth ₹50 lakh, the total payout after accidental death could become ₹1.5 crore. The rider amount is paid along with the base life insurance benefit.

This rider applies only when death occurs due to an accident. Natural causes or illnesses are not covered under it.

Some people consider it unnecessary. Others prefer having the additional protection because accidents are unpredictable and often financially disruptive for families.

Perspective matters here.

This rider becomes useful when the policyholder is no longer able to continue paying premiums.

If the insured person suffers a permanent disability or certain serious illnesses covered by the rider, the insurer waives all future premiums. The policyholder stops paying.

But the policy itself continues.

The life cover remains active exactly as before even though the insured person is no longer contributing premiums. The insurer effectively keeps the policy running under the original terms.

For people who are the primary earners in their family, this rider can quietly become one of the most valuable protections.

An accidental disability rider provides financial support if the policyholder becomes permanently disabled due to an accident.

Disability in this context may include:

Some policies offer a lump sum payout. Others provide periodic payments over several years.

These payments can help cover medical treatment, rehabilitation, and daily living expenses while the person adjusts to a new situation.

For people whose work depends heavily on physical mobility or manual effort, this rider can feel particularly relevant.

Riders in insurance can be useful. But not every rider fits every situation.

Raj realized this while going through the options. Instead of agreeing to everything the agent suggested, he started thinking about his own financial situation and the risks that realistically applied to him.

A few factors usually make the decision clearer.

If a family relies heavily on one person’s income, riders that protect against disability or serious illness become more relevant. Losing income for several months can create financial pressure quickly.

An additional payout during that period can help stabilize things.

Someone who travels frequently, drives long distances, or works in physically demanding environments might think more seriously about accidental riders.

These risks are sudden. Often unpredictable.

If someone already has a strong health insurance plan that includes critical illness coverage, adding the same protection through a rider may not always be necessary.

Sometimes riders in insurance simply duplicate benefits that already exist.

Not every rider is essential.

In fact, adding too many riders slowly increases the total premium of a policy. Each rider may seem affordable on its own, but the combined cost over decades can become noticeable.

There are situations where riders do not add much value.

For example:

In such cases keeping the base policy simple may actually make more sense.

Insurance works best when it protects against real financial risks. Not theoretical ones.

Some people wonder whether riders in insurance are better than buying separate insurance policies.

The answer depends on the situation.

| Feature | Insurance Rider | Separate Policy |

| Cost | Usually cheaper | Often more expensive |

| Coverage scope | Limited | More comprehensive |

| Flexibility | Linked to base policy | Independent policy |

| Claim structure | Simpler | May involve separate claim process |

Riders are typically cheaper because they extend an existing policy rather than creating a completely new one.

Standalone policies often provide broader protection and higher coverage limits. They may also offer more flexibility in terms of customization.

Many financial planners suggest a balanced approach.

Raj eventually added two riders to his policy. A critical illness rider and a waiver of premium rider. Not because someone insisted. Just because after thinking about it for a while, those two seemed practical enough for his situation.

Just like Raj if you need help with choosing your rider or fixing your finances, Finanjo is here for you!

Raj had just finished buying his first term policy without riders in insurance.

For a moment it felt oddly satisfying. Not exciting exactly. But there was a quiet sense of doing something responsible, something future-looking. The agent had explained the basics well enough. Pay the premium every year, keep the policy running, and if something happened to him during the policy term, the money would go to his family. Simple enough. Predictable. The sort of thing people tell themselves they will do someday, and then keep postponing.

Raj was about to close the laptop when the agent asked one more question.

“Would you like to add riders in insurance?”

He paused. The word sounded familiar but vague. Was this another policy? A feature? Or just one of those add-ons people agree to because the difference in premium seems small in the moment.

The agent began listing them. Critical illness rider. Accidental death rider. Waiver of premium rider.

Now Raj had mixed feelings. On one hand, each rider sounded practical. Life is messy and unpredictable after all. On the other hand, it felt like the simple policy he just understood was slowly turning into a menu of decisions he was not fully sure about.

That confusion is actually very common.

Many people buy a term plan and move on without ever really understanding riders in insurance. Some add every option suggested because the additional premium feels manageable. Others avoid them completely because the details feel confusing and the policy already seems complicated enough.

Usually the answer sits somewhere in between.

Understanding what riders really do, how they connect to a base insurance policy, and when they genuinely make sense can make the entire decision process a lot clearer. Not simpler perhaps, but clearer with Finanjo – experts for personal finance in India.

A rider is an additional benefit that can be attached to an existing insurance policy.

It slightly modifies the policy by adding protection for certain situations that may not be fully covered by the main policy. In most cases this comes with an additional cost that increases the annual premium by a small amount. Sometimes very small, which is exactly why riders often look tempting at the time of purchase.

Think of it as an extension to the base policy.

The core policy continues to provide its original protection exactly as promised. The rider simply expands the coverage by addressing specific risks that could happen during the policy period.

For example, someone buying a term life insurance policy might add a rider that provides an extra payout if death occurs due to an accident. Another rider may provide money if the insured person is diagnosed with a critical illness such as cancer or a serious heart condition.

These benefits sit on top of the main policy rather than replacing it. The original life cover remains intact. The riders in insurance just create an additional safety layer.

Insurance companies sometimes describe riders in insurance as optional. Which is technically true. But the decision about whether to add them usually depends on how someone thinks about risk, money, and uncertainty.

Well, to answer our Reddit friend we have an explanation here with a simple example.

Let us circle back to Raj. Suppose Raj buys a term insurance policy with these details.

| Component | Value |

| Base policy type | Term Life Insurance |

| Sum assured | ₹1 crore |

| Policy term | 30 years |

| Annual premium | ₹12,000 |

Now imagine he adds Critical Illness Riders in insurance worth ₹10 lakh.

The policy would look something like this.

| Component | Value |

| Base cover | ₹1 crore life cover |

| Critical illness rider cover | ₹10 lakh |

| Additional rider premium | ₹1,200 per year |

| Total annual premium | ₹13,200 |

If Raj passes away during the policy term, his family still receives the full ₹1 crore from the base policy. That part does not change. Riders in insurance do not reduce the core life cover.

But if he is diagnosed with a covered critical illness while the policy is active, the rider allows him to receive the ₹10 lakh payout earlier. During his lifetime.

This payout is separate from the death benefit.

In many policies the rider amount is paid once the illness is diagnosed and confirmed under the policy conditions. After that the money can be used however the policyholder wants. Hospital bills. Recovery costs. Lost income. Even everyday expenses that slowly pile up when someone is unable to work.

Sometimes people assume health insurance will handle everything. In reality there are always costs that slip through the cracks. Recovery periods. Lifestyle adjustments. Small things that quietly become expensive.

That is where riders in insurance often start making sense.

Insurance policies usually focus on broad categories of risk.

Life insurance covers death. Health insurance covers medical treatment. Disability policies address income loss due to injury or illness. Structuring policies this way keeps things organized and easier to explain.

But real life rarely follows those neat boundaries.

Certain risks overlap. Or fall awkwardly between categories. A serious illness might require expensive treatment while also preventing someone from working for months. Sometimes longer.

Situations like these expose gaps.

For example:

These problems are not always fully covered by a single insurance policy.

Riders in insurance exist to close those small but important gaps.

Instead of forcing people to purchase several separate insurance policies, insurers allow smaller protections to be attached directly to the base policy. It simplifies things a little. Or at least tries to.

And usually the cost is lower than buying a completely separate policy.

Still, just because something is available does not mean it is necessary for everyone.

Companies in India offer several riders in insurance. Some are very common across insurers while others depend on the company and the specific policy.

A few riders appear in most life insurance plans.

This rider provides a lump sum payout if the policyholder is diagnosed with certain serious illnesses.

Typically the list includes conditions like:

The payout is triggered once the illness is diagnosed and confirmed under the policy definitions. And those definitions matter. Insurance policies tend to be very specific about what qualifies as a claim.

The money can be used for treatment costs, recovery expenses, or income replacement during the illness period. Unlike health insurance, the payout is usually not tied to hospital bills. The insured person decides how to use it.

Many policyholders find that flexibility reassuring.

Critical illness riders are probably the most widely chosen riders with term insurance policies in India.

An accidental death rider provides an additional payout if death occurs due to an accident.

Suppose the base policy provides ₹1 crore cover.

If the policyholder has an accidental death rider worth ₹50 lakh, the total payout after accidental death could become ₹1.5 crore. The rider amount is paid along with the base life insurance benefit.

This rider applies only when death occurs due to an accident. Natural causes or illnesses are not covered under it.

Some people consider it unnecessary. Others prefer having the additional protection because accidents are unpredictable and often financially disruptive for families.

Perspective matters here.

This rider becomes useful when the policyholder is no longer able to continue paying premiums.

If the insured person suffers a permanent disability or certain serious illnesses covered by the rider, the insurer waives all future premiums. The policyholder stops paying.

But the policy itself continues.

The life cover remains active exactly as before even though the insured person is no longer contributing premiums. The insurer effectively keeps the policy running under the original terms.

For people who are the primary earners in their family, this rider can quietly become one of the most valuable protections.

An accidental disability rider provides financial support if the policyholder becomes permanently disabled due to an accident.

Disability in this context may include:

Some policies offer a lump sum payout. Others provide periodic payments over several years.

These payments can help cover medical treatment, rehabilitation, and daily living expenses while the person adjusts to a new situation.

For people whose work depends heavily on physical mobility or manual effort, this rider can feel particularly relevant.

Riders in insurance can be useful. But not every rider fits every situation.

Raj realized this while going through the options. Instead of agreeing to everything the agent suggested, he started thinking about his own financial situation and the risks that realistically applied to him.

A few factors usually make the decision clearer.

If a family relies heavily on one person’s income, riders that protect against disability or serious illness become more relevant. Losing income for several months can create financial pressure quickly.

An additional payout during that period can help stabilize things.

Someone who travels frequently, drives long distances, or works in physically demanding environments might think more seriously about accidental riders.

These risks are sudden. Often unpredictable.

If someone already has a strong health insurance plan that includes critical illness coverage, adding the same protection through a rider may not always be necessary.

Sometimes riders in insurance simply duplicate benefits that already exist.

Not every rider is essential.

In fact, adding too many riders slowly increases the total premium of a policy. Each rider may seem affordable on its own, but the combined cost over decades can become noticeable.

There are situations where riders do not add much value.

For example:

In such cases keeping the base policy simple may actually make more sense.

Insurance works best when it protects against real financial risks. Not theoretical ones.

Some people wonder whether riders in insurance are better than buying separate insurance policies.

The answer depends on the situation.

| Feature | Insurance Rider | Separate Policy |

| Cost | Usually cheaper | Often more expensive |

| Coverage scope | Limited | More comprehensive |

| Flexibility | Linked to base policy | Independent policy |

| Claim structure | Simpler | May involve separate claim process |

Riders are typically cheaper because they extend an existing policy rather than creating a completely new one.

Standalone policies often provide broader protection and higher coverage limits. They may also offer more flexibility in terms of customization.

Many financial planners suggest a balanced approach.

Raj eventually added two riders to his policy. A critical illness rider and a waiver of premium rider. Not because someone insisted. Just because after thinking about it for a while, those two seemed practical enough for his situation.

Just like Raj if you need help with choosing your rider or fixing your finances, Finanjo is here for you!

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.