At Finanjo, we spend a fair amount of time interacting with young professionals across India about money. Salary growth, investing, budgeting, taxes, life insurance, and health insurance. The typical topics.

But healthcare expenses come up far more often than people expect. Not at the start of the conversation. Usually somewhere in the middle, when someone casually mentions a hospital bill that felt… oddly high.

Sometimes it begins with a simple story.

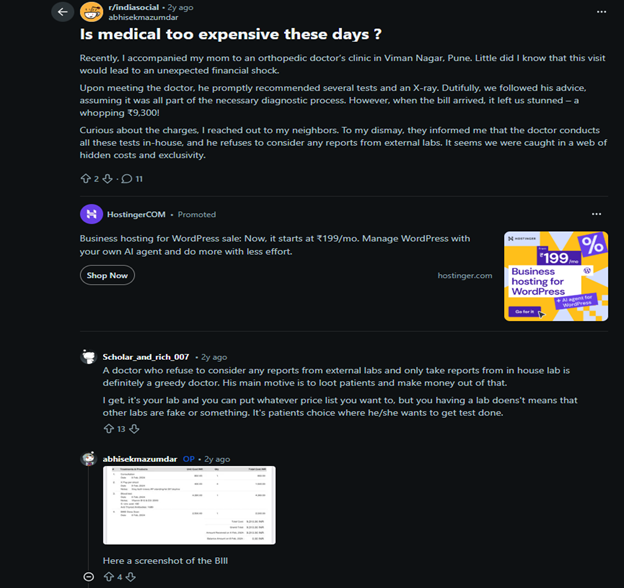

A Reddit user recently shared an experience from Pune. Their mother had been taken to an orthopedic clinic in Viman Nagar for what sounded like a routine consultation. Nothing urgent. No emergency situation. Just a visit to get a joint pain checked.

Most families walk into such appointments expecting predictable costs. Consultation. Maybe a prescription. Possibly a follow-up visit.

The doctor examined her and suggested a few diagnostic tests along with an X-ray. That recommendation did not feel unusual. Doctors rely heavily on diagnostic confirmation, and most patients rarely question those suggestions.

So the tests were done.

Then the bill arrived.

₹9,300.

Now, that number is not catastrophic. It does not destroy a household’s finances. But it is just high enough to make someone pause for a second and mentally replay what happened during the appointment.

A consultation. A few tests. An X-ray.

Situations like this appear more often than people admit. Someone goes in for a simple check-up. A couple of tests are suggested. A scan is added during the follow-up. Suddenly the bill feels heavier than expected.

Nothing dramatic happened. Yet the total climbed. Experiences like these linger in memory. Not because they cause immediate financial damage, but because they hint at a pattern.

Healthcare is getting more expensive. And it is happening quietly. Economists call this medical inflation.

Medical inflation simply refers to the rate at which healthcare costs increase over time. Hospital stays, medicines, surgeries, diagnostic tests. Almost every component of medical care becomes more expensive gradually.

The concept itself is easy to grasp. What surprises most people is the pace.

Healthcare costs do not rise at the same rate as everyday goods. In India, medical expenses tend to climb noticeably faster than general inflation.

Consultation fees creep upward every few years. Diagnostic tests become slightly more expensive. Hospitals invest in advanced equipment, larger facilities, and specialised staff. Those improvements are valuable. They are not cheap.

Eventually the cost shows up in patient bills. The change rarely feels dramatic in a single year. But stretch the timeline to ten or fifteen years and the numbers start behaving very differently.

A study by Aon estimated that healthcare costs in India have been rising at around 13 percent annually in recent years.

Another analysis from Willis Towers Watson placed India among the countries with the fastest rising medical expenses in Asia.

To see what that actually means, it helps to look at how treatment costs change over time.

| Treatment Cost Today | After 10 Years | After 15 Years | After 20 Years |

| ₹1 lakh | ₹2.59 lakh | ₹4.17 lakh | ₹6.72 lakh |

| ₹3 lakh | ₹7.78 lakh | ₹12.5 lakh | ₹20 lakh |

| ₹5 lakh | ₹12.9 lakh | ₹20.8 lakh | ₹33.6 lakh |

A procedure that costs ₹3 lakh today could approach ₹20 lakh two decades later. It looks simple on paper.

Real life rarely presents the numbers this neatly. Costs move unpredictably. Some treatments become cheaper with time. Others get far more expensive because new technology enters the picture.

But the direction of movement is rarely downward.

There is a tendency to assume hospitals simply charge more because they can. That explanation feels convenient, though it is not the whole story.

Healthcare costs rise for several overlapping reasons. Some of those reasons are actually positive developments.

Medical science has advanced quickly in the past twenty years. Diagnostic tools have improved. Surgeries are less invasive. Recovery times are shorter. Treatments exist today that would have sounded unrealistic not very long ago.

Progress in medicine tends to raise expectations. And expectations often raise costs. Hospitals operate complex ecosystems now. Advanced imaging equipment. Highly specialised doctors. Intensive care units that resemble miniature technology hubs.

Maintaining that infrastructure is expensive. Eventually those costs find their way into hospital bills.

| Driver | Example | Typical Cost Range | Impact |

| Diagnostic technology | MRI or CT scans | ₹5,000 – ₹30,000 | Higher testing expenses |

| Specialist consultations | Cardiology or neurology | ₹800 – ₹2,500 | Premium consultation fees |

| Long-term medication | Diabetes treatment | ₹3,000 – ₹8,000 monthly | Continuous spending |

| Advanced treatments | Cancer therapies | ₹50,000 – ₹2 lakh | Expensive treatment cycles |

| Private hospital infrastructure | ICU care | ₹25,000 – ₹75,000 per day | High inpatient costs |

Another factor quietly driving costs upward is lifestyle disease.

Conditions like diabetes, hypertension, and heart disease have become extremely common in urban India. These illnesses rarely disappear after one treatment. They demand monitoring, medication, tests, and regular consultations.

Sometimes for decades.

The Indian Council of Medical Research estimates that non-communicable diseases account for nearly 60 percent of deaths in India.

Treating these conditions over long periods naturally increases healthcare spending. Medical progress extends life expectancy. But longer lifespans also mean more years of medical management. That trade-off is rarely discussed openly.

Healthcare expenses behave differently from most other costs.

Rent arrives every month. Electricity bills follow a predictable pattern. Groceries fluctuate slightly but remain manageable. Medical expenses do not follow that rhythm. They appear suddenly.

A hospitalisation. A surgery. A late-night emergency visit. A diagnostic test that unexpectedly leads to another. When these situations occur, the financial impact can be immediate.

| Medical Procedure | Average Cost | Premium Hospital Cost | Typical Stay |

| Angioplasty | ₹2.5 lakh | ₹4.5 lakh | 2-4 days |

| Knee replacement | ₹3.5 lakh | ₹6 lakh | 4-7 days |

| Cataract surgery | ₹30,000 | ₹1.2 lakh | Same day |

| Chemotherapy cycle | ₹40,000 | ₹2 lakh | Multiple cycles |

| ICU stay | ₹25,000/day | ₹75,000/day | Varies |

A single hospitalisation can quietly erase years of careful saving.

According to the Public Health Foundation of India, more than half of healthcare spending in India is still paid directly by households rather than through insurance. That statistic explains a lot about why medical bills often feel overwhelming.

Anyone who has spent time inside a hospital billing office understands how quickly numbers accumulate. Tests. Medicines. Specialist consultations. Equipment usage.

Individually each line item looks manageable. Together they form a bill that demands attention.

Health insurance exists primarily to soften the financial shock associated with medical emergencies. Many professionals already receive some form of coverage through their employer. On the surface that sounds reassuring.

In practice, employer policies often have limitations. Coverage amounts may be modest. Some treatments have restrictions. Certain hospitals fall outside the network.

These details usually remain invisible until someone tries to use the policy.

That is why financial planners often suggest purchasing personal health insurance alongside employer coverage. The advice sounds straightforward.

Following it is slightly less straightforward. People postpone it. Sometimes for years.

| Situation | Without Insurance | With Insurance | Outcome |

| ₹3 lakh surgery | Paid entirely from savings | Covered by insurer | Savings remain intact |

| ICU stay for 5 days | ₹1.5 – ₹3 lakh expense | Mostly covered | Reduced financial stress |

| Emergency hospitalisation | Immediate payment required | Cashless treatment possible | Faster admission |

| Chronic disease treatment | Long-term personal spending | Partial coverage | Lower ongoing burden |

Insurance does not eliminate medical expenses.

It simply redistributes risk. Instead of one family absorbing the entire financial shock, the cost gets spread across a larger pool of policyholders through the insurer.

The Insurance Regulatory and Development Authority of India reports that health insurance penetration in India remains relatively low compared with many developed economies.

Which means a large portion of the population still relies on personal savings during medical emergencies. That strategy works until it does not.

Health insurance rarely feels urgent during the early stages of a career.

Most young professionals are healthy. Hospital visits are rare. Financial goals revolve around travel, gadgets, or upgrading apartments.

Healthcare planning quietly slides down the priority list. That reaction is understandable. It is also slightly risky. Buying insurance early offers a few practical advantages.

| Age | Annual Premium for ₹10L Cover | Medical Checks | Long-Term Advantage |

| 25 | ₹7,000 – ₹10,000 | Minimal | Lowest premiums |

| 30 | ₹9,000 – ₹14,000 | Basic checks | Affordable coverage |

| 40 | ₹18,000 – ₹30,000 | Detailed checks | Higher premiums |

| 50 | ₹35,000+ | Extensive checks | Limited options |

Premiums tend to increase with age. Waiting periods also complicate things. Many insurance policies require policyholders to wait several years before covering specific illnesses or treatments.

Starting earlier means those waiting periods quietly expire in the background. When coverage finally becomes useful, it is already active.

Eventually the conversation around health insurance becomes surprisingly practical.

People stop asking which policy looks attractive on paper. Instead they ask a more direct question.

Which insurer actually pays claims.

A Reddit discussion recently raised this exact concern. The user was not looking for the cheapest policy. They wanted to know which companies reliably approve claims rather than delaying them endlessly.

The conversation also touched on one common metric people rely on.

Claim Settlement Ratio, often called CSR.

At first glance the statistic seems reassuring. It shows the percentage of claims settled by an insurer in a year. A higher number appears better.

But numbers sometimes hide complexity.

A claim might technically be “settled” even if the insurer pays only part of the hospital bill. Statistically it counts as resolved. From the patient’s perspective the experience might feel slightly different.

Other metrics like complaint ratios exist as well. They provide hints, though they rarely capture the full picture.

| Metric | What It Indicates | Limitation |

| Claim Settlement Ratio | Percentage of claims settled | Includes partial settlements |

| Complaint Ratio | Complaints per claim | Hard to compare across insurers |

| Hospital Network | Number of cashless hospitals | Quality varies widely |

| Claim Processing Speed | Time taken to approve claims | Depends on hospital coordination |

Stories from policyholders often explain the reality better than statistics.

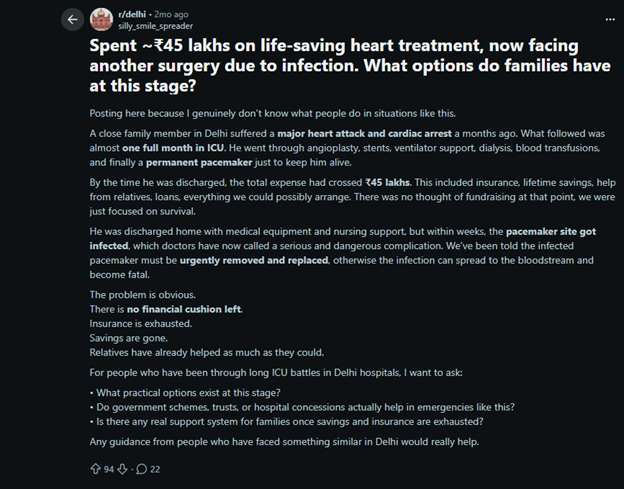

One example involved a patient who suddenly required heart treatment. The hospital estimated the procedure might cost around ₹45 lakh. The number was intimidating.

Then the hospital checked the patient’s insurance details and initiated a cashless request. Approval arrived within a few hours. Treatment moved forward immediately.

The patient recovered. The family did not have to liquidate their savings. That difference explains why reliability matters more than marketing brochures.

Medical inflation rarely dominate financial conversations. Stock market returns attract attention. Real estate prices trigger debates. Petrol prices somehow manage to enter dinner table discussions.

Medical expenses move quietly in the background. Hospitals expand. Diagnostic technology improves. Treatment options multiply. Bills grow alongside them.

Someone goes in for a consultation. A couple of tests follow. A scan appears in the next appointment. The numbers rise slowly enough that nobody notices the pattern immediately.

Then a hospitalisation happens. Suddenly the math becomes very clear.

This is where platforms like Finanjo spend most of their time helping young Indians make sense of their finances. Not just investments or savings goals. The less exciting parts too. Insurance planning, emergency funds, the quiet risks that rarely feel urgent until they are.

Money management is often portrayed as something complicated. Sometimes it is simply about preparing for the expenses people would rather not think about.

At Finanjo, we spend a fair amount of time interacting with young professionals across India about money. Salary growth, investing, budgeting, taxes, life insurance, and health insurance. The typical topics.

But healthcare expenses come up far more often than people expect. Not at the start of the conversation. Usually somewhere in the middle, when someone casually mentions a hospital bill that felt… oddly high.

Sometimes it begins with a simple story.

A Reddit user recently shared an experience from Pune. Their mother had been taken to an orthopedic clinic in Viman Nagar for what sounded like a routine consultation. Nothing urgent. No emergency situation. Just a visit to get a joint pain checked.

Most families walk into such appointments expecting predictable costs. Consultation. Maybe a prescription. Possibly a follow-up visit.

The doctor examined her and suggested a few diagnostic tests along with an X-ray. That recommendation did not feel unusual. Doctors rely heavily on diagnostic confirmation, and most patients rarely question those suggestions.

So the tests were done.

Then the bill arrived.

₹9,300.

Now, that number is not catastrophic. It does not destroy a household’s finances. But it is just high enough to make someone pause for a second and mentally replay what happened during the appointment.

A consultation. A few tests. An X-ray.

Situations like this appear more often than people admit. Someone goes in for a simple check-up. A couple of tests are suggested. A scan is added during the follow-up. Suddenly the bill feels heavier than expected.

Nothing dramatic happened. Yet the total climbed. Experiences like these linger in memory. Not because they cause immediate financial damage, but because they hint at a pattern.

Healthcare is getting more expensive. And it is happening quietly. Economists call this medical inflation.

Medical inflation simply refers to the rate at which healthcare costs increase over time. Hospital stays, medicines, surgeries, diagnostic tests. Almost every component of medical care becomes more expensive gradually.

The concept itself is easy to grasp. What surprises most people is the pace.

Healthcare costs do not rise at the same rate as everyday goods. In India, medical expenses tend to climb noticeably faster than general inflation.

Consultation fees creep upward every few years. Diagnostic tests become slightly more expensive. Hospitals invest in advanced equipment, larger facilities, and specialised staff. Those improvements are valuable. They are not cheap.

Eventually the cost shows up in patient bills. The change rarely feels dramatic in a single year. But stretch the timeline to ten or fifteen years and the numbers start behaving very differently.

A study by Aon estimated that healthcare costs in India have been rising at around 13 percent annually in recent years.

Another analysis from Willis Towers Watson placed India among the countries with the fastest rising medical expenses in Asia.

To see what that actually means, it helps to look at how treatment costs change over time.

| Treatment Cost Today | After 10 Years | After 15 Years | After 20 Years |

| ₹1 lakh | ₹2.59 lakh | ₹4.17 lakh | ₹6.72 lakh |

| ₹3 lakh | ₹7.78 lakh | ₹12.5 lakh | ₹20 lakh |

| ₹5 lakh | ₹12.9 lakh | ₹20.8 lakh | ₹33.6 lakh |

A procedure that costs ₹3 lakh today could approach ₹20 lakh two decades later. It looks simple on paper.

Real life rarely presents the numbers this neatly. Costs move unpredictably. Some treatments become cheaper with time. Others get far more expensive because new technology enters the picture.

But the direction of movement is rarely downward.

There is a tendency to assume hospitals simply charge more because they can. That explanation feels convenient, though it is not the whole story.

Healthcare costs rise for several overlapping reasons. Some of those reasons are actually positive developments.

Medical science has advanced quickly in the past twenty years. Diagnostic tools have improved. Surgeries are less invasive. Recovery times are shorter. Treatments exist today that would have sounded unrealistic not very long ago.

Progress in medicine tends to raise expectations. And expectations often raise costs. Hospitals operate complex ecosystems now. Advanced imaging equipment. Highly specialised doctors. Intensive care units that resemble miniature technology hubs.

Maintaining that infrastructure is expensive. Eventually those costs find their way into hospital bills.

| Driver | Example | Typical Cost Range | Impact |

| Diagnostic technology | MRI or CT scans | ₹5,000 – ₹30,000 | Higher testing expenses |

| Specialist consultations | Cardiology or neurology | ₹800 – ₹2,500 | Premium consultation fees |

| Long-term medication | Diabetes treatment | ₹3,000 – ₹8,000 monthly | Continuous spending |

| Advanced treatments | Cancer therapies | ₹50,000 – ₹2 lakh | Expensive treatment cycles |

| Private hospital infrastructure | ICU care | ₹25,000 – ₹75,000 per day | High inpatient costs |

Another factor quietly driving costs upward is lifestyle disease.

Conditions like diabetes, hypertension, and heart disease have become extremely common in urban India. These illnesses rarely disappear after one treatment. They demand monitoring, medication, tests, and regular consultations.

Sometimes for decades.

The Indian Council of Medical Research estimates that non-communicable diseases account for nearly 60 percent of deaths in India.

Treating these conditions over long periods naturally increases healthcare spending. Medical progress extends life expectancy. But longer lifespans also mean more years of medical management. That trade-off is rarely discussed openly.

Healthcare expenses behave differently from most other costs.

Rent arrives every month. Electricity bills follow a predictable pattern. Groceries fluctuate slightly but remain manageable. Medical expenses do not follow that rhythm. They appear suddenly.

A hospitalisation. A surgery. A late-night emergency visit. A diagnostic test that unexpectedly leads to another. When these situations occur, the financial impact can be immediate.

| Medical Procedure | Average Cost | Premium Hospital Cost | Typical Stay |

| Angioplasty | ₹2.5 lakh | ₹4.5 lakh | 2-4 days |

| Knee replacement | ₹3.5 lakh | ₹6 lakh | 4-7 days |

| Cataract surgery | ₹30,000 | ₹1.2 lakh | Same day |

| Chemotherapy cycle | ₹40,000 | ₹2 lakh | Multiple cycles |

| ICU stay | ₹25,000/day | ₹75,000/day | Varies |

A single hospitalisation can quietly erase years of careful saving.

According to the Public Health Foundation of India, more than half of healthcare spending in India is still paid directly by households rather than through insurance. That statistic explains a lot about why medical bills often feel overwhelming.

Anyone who has spent time inside a hospital billing office understands how quickly numbers accumulate. Tests. Medicines. Specialist consultations. Equipment usage.

Individually each line item looks manageable. Together they form a bill that demands attention.

Health insurance exists primarily to soften the financial shock associated with medical emergencies. Many professionals already receive some form of coverage through their employer. On the surface that sounds reassuring.

In practice, employer policies often have limitations. Coverage amounts may be modest. Some treatments have restrictions. Certain hospitals fall outside the network.

These details usually remain invisible until someone tries to use the policy.

That is why financial planners often suggest purchasing personal health insurance alongside employer coverage. The advice sounds straightforward.

Following it is slightly less straightforward. People postpone it. Sometimes for years.

| Situation | Without Insurance | With Insurance | Outcome |

| ₹3 lakh surgery | Paid entirely from savings | Covered by insurer | Savings remain intact |

| ICU stay for 5 days | ₹1.5 – ₹3 lakh expense | Mostly covered | Reduced financial stress |

| Emergency hospitalisation | Immediate payment required | Cashless treatment possible | Faster admission |

| Chronic disease treatment | Long-term personal spending | Partial coverage | Lower ongoing burden |

Insurance does not eliminate medical expenses.

It simply redistributes risk. Instead of one family absorbing the entire financial shock, the cost gets spread across a larger pool of policyholders through the insurer.

The Insurance Regulatory and Development Authority of India reports that health insurance penetration in India remains relatively low compared with many developed economies.

Which means a large portion of the population still relies on personal savings during medical emergencies. That strategy works until it does not.

Health insurance rarely feels urgent during the early stages of a career.

Most young professionals are healthy. Hospital visits are rare. Financial goals revolve around travel, gadgets, or upgrading apartments.

Healthcare planning quietly slides down the priority list. That reaction is understandable. It is also slightly risky. Buying insurance early offers a few practical advantages.

| Age | Annual Premium for ₹10L Cover | Medical Checks | Long-Term Advantage |

| 25 | ₹7,000 – ₹10,000 | Minimal | Lowest premiums |

| 30 | ₹9,000 – ₹14,000 | Basic checks | Affordable coverage |

| 40 | ₹18,000 – ₹30,000 | Detailed checks | Higher premiums |

| 50 | ₹35,000+ | Extensive checks | Limited options |

Premiums tend to increase with age. Waiting periods also complicate things. Many insurance policies require policyholders to wait several years before covering specific illnesses or treatments.

Starting earlier means those waiting periods quietly expire in the background. When coverage finally becomes useful, it is already active.

Eventually the conversation around health insurance becomes surprisingly practical.

People stop asking which policy looks attractive on paper. Instead they ask a more direct question.

Which insurer actually pays claims.

A Reddit discussion recently raised this exact concern. The user was not looking for the cheapest policy. They wanted to know which companies reliably approve claims rather than delaying them endlessly.

The conversation also touched on one common metric people rely on.

Claim Settlement Ratio, often called CSR.

At first glance the statistic seems reassuring. It shows the percentage of claims settled by an insurer in a year. A higher number appears better.

But numbers sometimes hide complexity.

A claim might technically be “settled” even if the insurer pays only part of the hospital bill. Statistically it counts as resolved. From the patient’s perspective the experience might feel slightly different.

Other metrics like complaint ratios exist as well. They provide hints, though they rarely capture the full picture.

| Metric | What It Indicates | Limitation |

| Claim Settlement Ratio | Percentage of claims settled | Includes partial settlements |

| Complaint Ratio | Complaints per claim | Hard to compare across insurers |

| Hospital Network | Number of cashless hospitals | Quality varies widely |

| Claim Processing Speed | Time taken to approve claims | Depends on hospital coordination |

Stories from policyholders often explain the reality better than statistics.

One example involved a patient who suddenly required heart treatment. The hospital estimated the procedure might cost around ₹45 lakh. The number was intimidating.

Then the hospital checked the patient’s insurance details and initiated a cashless request. Approval arrived within a few hours. Treatment moved forward immediately.

The patient recovered. The family did not have to liquidate their savings. That difference explains why reliability matters more than marketing brochures.

Medical inflation rarely dominate financial conversations. Stock market returns attract attention. Real estate prices trigger debates. Petrol prices somehow manage to enter dinner table discussions.

Medical expenses move quietly in the background. Hospitals expand. Diagnostic technology improves. Treatment options multiply. Bills grow alongside them.

Someone goes in for a consultation. A couple of tests follow. A scan appears in the next appointment. The numbers rise slowly enough that nobody notices the pattern immediately.

Then a hospitalisation happens. Suddenly the math becomes very clear.

This is where platforms like Finanjo spend most of their time helping young Indians make sense of their finances. Not just investments or savings goals. The less exciting parts too. Insurance planning, emergency funds, the quiet risks that rarely feel urgent until they are.

Money management is often portrayed as something complicated. Sometimes it is simply about preparing for the expenses people would rather not think about.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.