Shubham had just received his first meaningful annual bonus. Not the kind of money that makes someone quit their job or suddenly plan a Euro trip. Still, it was enough to make him stare at his bank balance a little longer that evening, but life insurance did not cross his mind.

For the first time in a while, the number sitting there did not feel like it was about to disappear in a week. Earlier, his salary would arrive like a surprise cameo by SRK. Big moment, lots of excitement, and then gone before you fully process it.

Rent would immediately take its share. EMIs would quietly line up in the background like they always do. Swiggy would do what it always does during late-night hunger pangs when you are tired after work, and the idea of cooking feels like unnecessary effort. A few random online purchases would sneak in as well.

By the end of the month, the balance usually returned to its natural habitat. Slightly alarming territory where the UPI app suddenly feels very personal. You start checking it more often than you want to admit.

This time it stayed.

The first instinct rarely involves insurance, though. Shubham briefly thought about upgrading his phone and even looked at a few travel deals. Someone at work had been talking about mutual fund SIPs during lunch breaks, so he opened a couple of investment articles as well.

Insurance did not appear in that list.

That changed one evening when his father casually asked during dinner whether he had taken life insurance yet. It sounded like a simple question. The kind parents ask in passing. But it stayed in his head longer than expected.

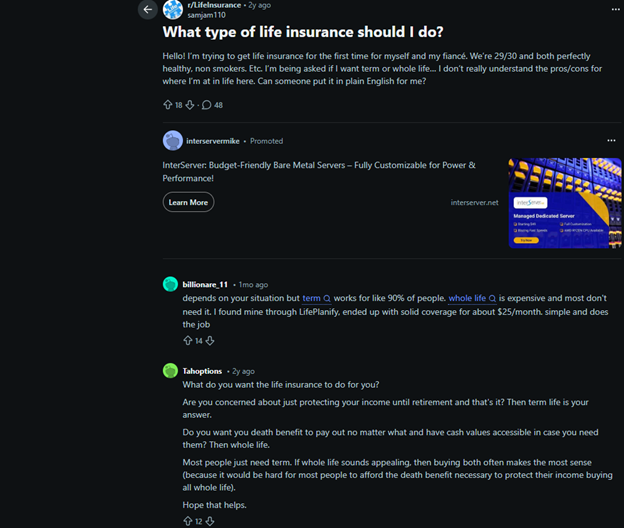

Once Shubham started looking into it, the simplicity disappeared almost immediately. Life insurance in India does not come as one product. It arrives as a long list. Term plans, endowment plans, ULIPs, money-back policies, and whole life insurance.

Every explanation sounded convincing. Almost too convincing, actually. You can feel the sales pitch hiding behind some of the descriptions.

Soon, the real problem appeared. There were too many options, trying to do too many things at once. Protection, investment, savings, tax benefits. For someone who just wanted a clear answer, the information overload built pretty quickly.

That is usually the moment people wish someone would simply explain things without the financial jargon. Which is more or less what Finanjo tries to do. Make finance less confusing and help people like Shubham figure out what actually makes sense before buying something they only half understand.

At 25, Shubham did not spend a lot of time thinking about financial risk. Life felt reasonably sorted. His health was good, his job had finally started feeling stable, and his career seemed to be moving in the right direction. The future looked like one of those neat Excel projections where income slowly increases and responsibilities politely arrive one at a time.

Insurance, in his mind, belonged to a later stage of life. Somewhere in the same category as buying a house, worrying about cholesterol levels, or discussing mutual funds seriously at family weddings.

Real life rarely follows such tidy timelines, though. Anyone who has handled real expenses knows that.

Shubham still had an education loan quietly running in the background every month. His parents had also begun asking for small help with household expenses here and there. A medical bill one month, a home repair the next, maybe a festival expense that appeared out of nowhere.

Individually, none of it felt heavy. Together, though, it slowly changed something important. His salary was no longer just funding weekend plans, food deliveries, and occasional impulse shopping. Other people had started depending on it, too.

You notice that shift quietly. No dramatic moment. Just small realisations.

That is usually the moment financial protection begins to make more sense.

For someone like Shubham, the most valuable financial asset is not the money already sitting in his bank account. That number is still modest. The real asset is his future income over the next 30-35 years. Every salary credit, every promotion, every increment that will come over time.

That steady stream of earnings is what supports loans, family expenses, and long-term plans.

If that income suddenly disappears, the entire financial structure around it can wobble pretty quickly. It is not a pleasant thought, which is probably why most people avoid thinking about it for as long as possible.

According to the Insurance Regulatory and Development Authority of India, life insurance penetration in India was around 3.2 per cent of GDP in FY2023. In simple terms, a large number of working professionals still do not have adequate financial protection in place.

In India, people often realise the importance of insurance slightly later. Usually, after a few responsibilities show up. Or after one very persistent parent asks the same question every few weeks. Shubham had recently entered that phase.

Another study offers a more personal perspective. The India Protection Quotient report by Max Life Insurance and Kantar found that nearly 63 per cent of urban Indian households believe they would struggle financially if the primary earner were no longer around.

People recognise the risk intellectually. Acting on that recognition often takes time.

Shubham noticed the same pattern during his research. Many people his age understood the importance of financial protection, but delayed the decision because insurance felt complicated.

Once he decided to explore the topic seriously, the next question naturally followed – What types of life insurance plans actually exist?

When Shubham first searched for life insurance policies, he expected to see two or three simple options. Instead, he discovered an entire list of products designed for different financial objectives.

The options included term insurance, endowment plans, money-back policies, ULIPs, and whole life insurance. Each one appeared useful in its own way, but each one also served a slightly different purpose.

The confusion often begins with a simple assumption. Many people believe every insurance policy tries to achieve the same goal. In reality, different policies exist to solve very different financial problems.

Some policies focus purely on protecting income. Others combine insurance with savings. A few combine insurance with investments in financial markets.

Once Shubham understood that each plan solved a different problem, the structure became easier to follow. Slowly, at least.

Term insurance was the first product Shubham encountered during his research. It is also the simplest form of life insurance available in the market.

In a term insurance policy, the policyholder pays a fixed premium for a specific number of years. If the insured individual passes away during the policy period, the nominee receives the sum assured.

If the policyholder survives the policy term, the plan simply ends without a maturity payout. This part initially surprised Shubham because he assumed every insurance policy returned money at the end.

The absence of a maturity benefit is exactly what keeps term insurance affordable.

Since the policy focuses only on protection, the premium remains much lower than other types of life insurance.

| Feature | Explanation |

| Pure life cover | The policy focuses only on financial protection for the insured person’s life |

| Lower premiums | Because there is no investment or savings component, premiums remain affordable |

| Flexible tenure | Coverage can extend for long durations, such as 25 to 35 years |

| High sum assured | extensive coverage amounts like ₹1 crore are common |

For someone in his mid-twenties, Shubham realised that a one-crore policy might cost less per year than several lifestyle expenses he barely noticed. Streaming subscriptions, a few weekend outings, or a short trip could easily exceed the premium.

Once you notice that comparison, it becomes hard to ignore.

This affordability has made term insurance increasingly popular among younger buyers.

Endowment policies combine insurance with long-term savings. In these plans, the nominee receives the sum assured if the insured individual passes away during the policy term.

If the policyholder survives the term, the insurer pays a maturity amount along with bonuses accumulated during the policy period. This structure appeals to many households because it guarantees some financial return even if the policy completes its duration.

Shubham initially found the concept comforting because it resembled disciplined savings combined with life protection.

| Feature | Explanation |

| Insurance plus savings | Combines financial protection with long-term wealth accumulation |

| Guaranteed maturity payout | Policyholders receive the sum assured at the end of the policy term |

| Bonus participation | Insurers may add bonuses depending on the company’s performance |

| Savings discipline | Regular premium payments encourage long-term financial discipline |

The trade-off appears quickly, though. Because the policy combines savings with insurance protection, the premiums are significantly higher compared to term insurance.

And that difference becomes quite visible when you start comparing numbers.

Money-back policies resemble endowment plans but introduce periodic payouts during the policy period. Instead of receiving the entire amount at maturity, the policyholder receives portions of the sum assured at specific intervals.

These payouts are called survival benefits.

| Policy Year | Survival Benefit |

| Year 5 | 20 % of the sum assured |

| Year 10 | 20 % of the sum assured |

| Year 15 | 20 % of the sum assured |

| Maturity | Remaining amount plus bonuses |

This structure can help households manage predictable financial expenses such as education costs or home improvements. However, early payouts reduce the final maturity amount.

Premiums also remain relatively high because the insurer must manage multiple benefit payments during the policy period.

We do not want you to have this experience. So, we will break it down for you.

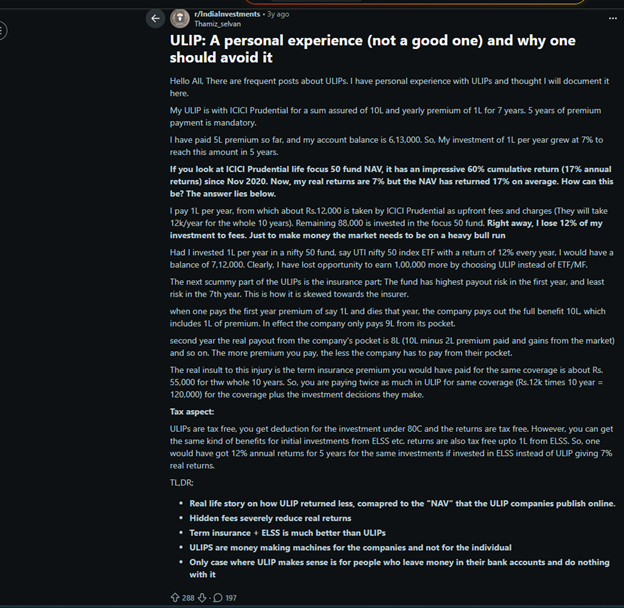

Unit Linked Insurance Plans combine life insurance with market investments. A portion of the premium pays for life insurance coverage, while the remaining amount gets invested in financial markets.

Policyholders usually choose between equity funds, debt funds, or balanced portfolios depending on their risk appetite.

| Component | Purpose |

| Mortality charge | Pays for life insurance coverage |

| Equity funds | Invests in stock market instruments |

| Debt funds | Invests in bonds and fixed income securities |

| Balanced funds | Mix of equity and debt investments |

Returns depend on market performance. Long-term equity investments in India have historically delivered returns of around 12 to 15 % annually, according to industry estimates.

However, ULIPs also include charges such as fund management fees, administrative costs, and mortality charges that affect overall returns.

Whole life insurance provides coverage for the entire lifetime of the insured individual. Instead of ending after a fixed term, these policies can remain active until the insured reaches advanced ages, such as ninety-nine.

These policies often support long-term wealth transfer and legacy planning.

| Feature | Explanation |

| Lifetime protection | Coverage continues throughout the insured person’s life |

| Cash value accumulation | Some policies gradually build savings value |

| Legacy planning | Benefits can be transferred to future generations |

| Long-term commitment | Premium structures often extend for decades |

For someone at Shubham’s stage of life, such long-term planning still felt distant. His immediate priorities involved protecting income while keeping financial flexibility intact.

Seeing all the plans together helped Shubham understand the bigger picture. Each product solves a different financial need rather than competing with one another.

| Insurance Plan | Primary Purpose | Premium Level | Maturity Benefit | Investment Component | Typical Suitability |

| Term Insurance | Pure protection | Low | No | None | Young professionals |

| Endowment Plan | Savings plus protection | High | Yes | Limited | Conservative savers |

| Money-Back Plan | Periodic payouts | High | Partial | Limited | Families needing liquidity |

| ULIP | Investment plus insurance | Moderate to high | Market linked | Yes | Market aware investors |

| Whole Life Plan | Lifetime protection | Moderate | Possible | Limited | Legacy planning |

Looking at the table, Shubham realised something simple. Every policy exists for a specific purpose. Confusion arises when people expect a single product to handle protection, investment, and savings simultaneously.

Young professionals like Shubham usually operate in a specific financial stage. Income is still stabilising, career paths may change, and major life decisions often remain a few years away.

Flexibility becomes valuable during this period.

Many financial planners, therefore, suggest starting with term insurance because it offers strong protection without locking too much money into long-term commitments.

| Advantage | Explanation |

| Lower premiums | Affordable during early career years |

| Large coverage | Protects family income effectively |

| Financial flexibility | The remaining income can be invested elsewhere |

| Simple structure | Easy to understand and manage |

Separating insurance from investments often simplifies financial planning. Insurance protects against risk while investments focus on wealth creation.

Personal finance rarely follows the same rules for everyone, though. Some individuals prefer guaranteed savings while others are comfortable with market exposure.

Different preferences lead to different choices, and financial planning usually evolves slowly as income and responsibilities grow. That is also where platforms like Finanjo try to make things simpler. Instead of overwhelming young earners with dozens of financial products, the goal is to help people like Shubham sort their finances step by step and understand what actually fits their stage of life.

Shubham had just received his first meaningful annual bonus. Not the kind of money that makes someone quit their job or suddenly plan a Euro trip. Still, it was enough to make him stare at his bank balance a little longer that evening, but life insurance did not cross his mind.

For the first time in a while, the number sitting there did not feel like it was about to disappear in a week. Earlier, his salary would arrive like a surprise cameo by SRK. Big moment, lots of excitement, and then gone before you fully process it.

Rent would immediately take its share. EMIs would quietly line up in the background like they always do. Swiggy would do what it always does during late-night hunger pangs when you are tired after work, and the idea of cooking feels like unnecessary effort. A few random online purchases would sneak in as well.

By the end of the month, the balance usually returned to its natural habitat. Slightly alarming territory where the UPI app suddenly feels very personal. You start checking it more often than you want to admit.

This time it stayed.

The first instinct rarely involves insurance, though. Shubham briefly thought about upgrading his phone and even looked at a few travel deals. Someone at work had been talking about mutual fund SIPs during lunch breaks, so he opened a couple of investment articles as well.

Insurance did not appear in that list.

That changed one evening when his father casually asked during dinner whether he had taken life insurance yet. It sounded like a simple question. The kind parents ask in passing. But it stayed in his head longer than expected.

Once Shubham started looking into it, the simplicity disappeared almost immediately. Life insurance in India does not come as one product. It arrives as a long list. Term plans, endowment plans, ULIPs, money-back policies, and whole life insurance.

Every explanation sounded convincing. Almost too convincing, actually. You can feel the sales pitch hiding behind some of the descriptions.

Soon, the real problem appeared. There were too many options, trying to do too many things at once. Protection, investment, savings, tax benefits. For someone who just wanted a clear answer, the information overload built pretty quickly.

That is usually the moment people wish someone would simply explain things without the financial jargon. Which is more or less what Finanjo tries to do. Make finance less confusing and help people like Shubham figure out what actually makes sense before buying something they only half understand.

At 25, Shubham did not spend a lot of time thinking about financial risk. Life felt reasonably sorted. His health was good, his job had finally started feeling stable, and his career seemed to be moving in the right direction. The future looked like one of those neat Excel projections where income slowly increases and responsibilities politely arrive one at a time.

Insurance, in his mind, belonged to a later stage of life. Somewhere in the same category as buying a house, worrying about cholesterol levels, or discussing mutual funds seriously at family weddings.

Real life rarely follows such tidy timelines, though. Anyone who has handled real expenses knows that.

Shubham still had an education loan quietly running in the background every month. His parents had also begun asking for small help with household expenses here and there. A medical bill one month, a home repair the next, maybe a festival expense that appeared out of nowhere.

Individually, none of it felt heavy. Together, though, it slowly changed something important. His salary was no longer just funding weekend plans, food deliveries, and occasional impulse shopping. Other people had started depending on it, too.

You notice that shift quietly. No dramatic moment. Just small realisations.

That is usually the moment financial protection begins to make more sense.

For someone like Shubham, the most valuable financial asset is not the money already sitting in his bank account. That number is still modest. The real asset is his future income over the next 30-35 years. Every salary credit, every promotion, every increment that will come over time.

That steady stream of earnings is what supports loans, family expenses, and long-term plans.

If that income suddenly disappears, the entire financial structure around it can wobble pretty quickly. It is not a pleasant thought, which is probably why most people avoid thinking about it for as long as possible.

According to the Insurance Regulatory and Development Authority of India, life insurance penetration in India was around 3.2 per cent of GDP in FY2023. In simple terms, a large number of working professionals still do not have adequate financial protection in place.

In India, people often realise the importance of insurance slightly later. Usually, after a few responsibilities show up. Or after one very persistent parent asks the same question every few weeks. Shubham had recently entered that phase.

Another study offers a more personal perspective. The India Protection Quotient report by Max Life Insurance and Kantar found that nearly 63 per cent of urban Indian households believe they would struggle financially if the primary earner were no longer around.

People recognise the risk intellectually. Acting on that recognition often takes time.

Shubham noticed the same pattern during his research. Many people his age understood the importance of financial protection, but delayed the decision because insurance felt complicated.

Once he decided to explore the topic seriously, the next question naturally followed – What types of life insurance plans actually exist?

When Shubham first searched for life insurance policies, he expected to see two or three simple options. Instead, he discovered an entire list of products designed for different financial objectives.

The options included term insurance, endowment plans, money-back policies, ULIPs, and whole life insurance. Each one appeared useful in its own way, but each one also served a slightly different purpose.

The confusion often begins with a simple assumption. Many people believe every insurance policy tries to achieve the same goal. In reality, different policies exist to solve very different financial problems.

Some policies focus purely on protecting income. Others combine insurance with savings. A few combine insurance with investments in financial markets.

Once Shubham understood that each plan solved a different problem, the structure became easier to follow. Slowly, at least.

Term insurance was the first product Shubham encountered during his research. It is also the simplest form of life insurance available in the market.

In a term insurance policy, the policyholder pays a fixed premium for a specific number of years. If the insured individual passes away during the policy period, the nominee receives the sum assured.

If the policyholder survives the policy term, the plan simply ends without a maturity payout. This part initially surprised Shubham because he assumed every insurance policy returned money at the end.

The absence of a maturity benefit is exactly what keeps term insurance affordable.

Since the policy focuses only on protection, the premium remains much lower than other types of life insurance.

| Feature | Explanation |

| Pure life cover | The policy focuses only on financial protection for the insured person’s life |

| Lower premiums | Because there is no investment or savings component, premiums remain affordable |

| Flexible tenure | Coverage can extend for long durations, such as 25 to 35 years |

| High sum assured | extensive coverage amounts like ₹1 crore are common |

For someone in his mid-twenties, Shubham realised that a one-crore policy might cost less per year than several lifestyle expenses he barely noticed. Streaming subscriptions, a few weekend outings, or a short trip could easily exceed the premium.

Once you notice that comparison, it becomes hard to ignore.

This affordability has made term insurance increasingly popular among younger buyers.

Endowment policies combine insurance with long-term savings. In these plans, the nominee receives the sum assured if the insured individual passes away during the policy term.

If the policyholder survives the term, the insurer pays a maturity amount along with bonuses accumulated during the policy period. This structure appeals to many households because it guarantees some financial return even if the policy completes its duration.

Shubham initially found the concept comforting because it resembled disciplined savings combined with life protection.

| Feature | Explanation |

| Insurance plus savings | Combines financial protection with long-term wealth accumulation |

| Guaranteed maturity payout | Policyholders receive the sum assured at the end of the policy term |

| Bonus participation | Insurers may add bonuses depending on the company’s performance |

| Savings discipline | Regular premium payments encourage long-term financial discipline |

The trade-off appears quickly, though. Because the policy combines savings with insurance protection, the premiums are significantly higher compared to term insurance.

And that difference becomes quite visible when you start comparing numbers.

Money-back policies resemble endowment plans but introduce periodic payouts during the policy period. Instead of receiving the entire amount at maturity, the policyholder receives portions of the sum assured at specific intervals.

These payouts are called survival benefits.

| Policy Year | Survival Benefit |

| Year 5 | 20 % of the sum assured |

| Year 10 | 20 % of the sum assured |

| Year 15 | 20 % of the sum assured |

| Maturity | Remaining amount plus bonuses |

This structure can help households manage predictable financial expenses such as education costs or home improvements. However, early payouts reduce the final maturity amount.

Premiums also remain relatively high because the insurer must manage multiple benefit payments during the policy period.

We do not want you to have this experience. So, we will break it down for you.

Unit Linked Insurance Plans combine life insurance with market investments. A portion of the premium pays for life insurance coverage, while the remaining amount gets invested in financial markets.

Policyholders usually choose between equity funds, debt funds, or balanced portfolios depending on their risk appetite.

| Component | Purpose |

| Mortality charge | Pays for life insurance coverage |

| Equity funds | Invests in stock market instruments |

| Debt funds | Invests in bonds and fixed income securities |

| Balanced funds | Mix of equity and debt investments |

Returns depend on market performance. Long-term equity investments in India have historically delivered returns of around 12 to 15 % annually, according to industry estimates.

However, ULIPs also include charges such as fund management fees, administrative costs, and mortality charges that affect overall returns.

Whole life insurance provides coverage for the entire lifetime of the insured individual. Instead of ending after a fixed term, these policies can remain active until the insured reaches advanced ages, such as ninety-nine.

These policies often support long-term wealth transfer and legacy planning.

| Feature | Explanation |

| Lifetime protection | Coverage continues throughout the insured person’s life |

| Cash value accumulation | Some policies gradually build savings value |

| Legacy planning | Benefits can be transferred to future generations |

| Long-term commitment | Premium structures often extend for decades |

For someone at Shubham’s stage of life, such long-term planning still felt distant. His immediate priorities involved protecting income while keeping financial flexibility intact.

Seeing all the plans together helped Shubham understand the bigger picture. Each product solves a different financial need rather than competing with one another.

| Insurance Plan | Primary Purpose | Premium Level | Maturity Benefit | Investment Component | Typical Suitability |

| Term Insurance | Pure protection | Low | No | None | Young professionals |

| Endowment Plan | Savings plus protection | High | Yes | Limited | Conservative savers |

| Money-Back Plan | Periodic payouts | High | Partial | Limited | Families needing liquidity |

| ULIP | Investment plus insurance | Moderate to high | Market linked | Yes | Market aware investors |

| Whole Life Plan | Lifetime protection | Moderate | Possible | Limited | Legacy planning |

Looking at the table, Shubham realised something simple. Every policy exists for a specific purpose. Confusion arises when people expect a single product to handle protection, investment, and savings simultaneously.

Young professionals like Shubham usually operate in a specific financial stage. Income is still stabilising, career paths may change, and major life decisions often remain a few years away.

Flexibility becomes valuable during this period.

Many financial planners, therefore, suggest starting with term insurance because it offers strong protection without locking too much money into long-term commitments.

| Advantage | Explanation |

| Lower premiums | Affordable during early career years |

| Large coverage | Protects family income effectively |

| Financial flexibility | The remaining income can be invested elsewhere |

| Simple structure | Easy to understand and manage |

Separating insurance from investments often simplifies financial planning. Insurance protects against risk while investments focus on wealth creation.

Personal finance rarely follows the same rules for everyone, though. Some individuals prefer guaranteed savings while others are comfortable with market exposure.

Different preferences lead to different choices, and financial planning usually evolves slowly as income and responsibilities grow. That is also where platforms like Finanjo try to make things simpler. Instead of overwhelming young earners with dozens of financial products, the goal is to help people like Shubham sort their finances step by step and understand what actually fits their stage of life.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.

A contributor to the Finanjo blog, where I share insightful and easy-to-understand content focused on educating readers about finance. With a clear and approachable writing style, I simplify complex topics to make them more understandable.